IMF to engage next govt before finalising loan review

The International Monetary Fund (IMF) will engage with the next government before finalising the upcoming loan review for Bangladesh, said Chris Papageorgiou, IMF mission chief to Bangladesh.Speaking at a virtual press conference yesterday, Papageorgiou said discussions with the authorities would continue."The newly elected authorities, which we are expecting to come into place in February [next year], [will] have an important say in them [IMF reform proposals]," he said."So, the plan is that we...

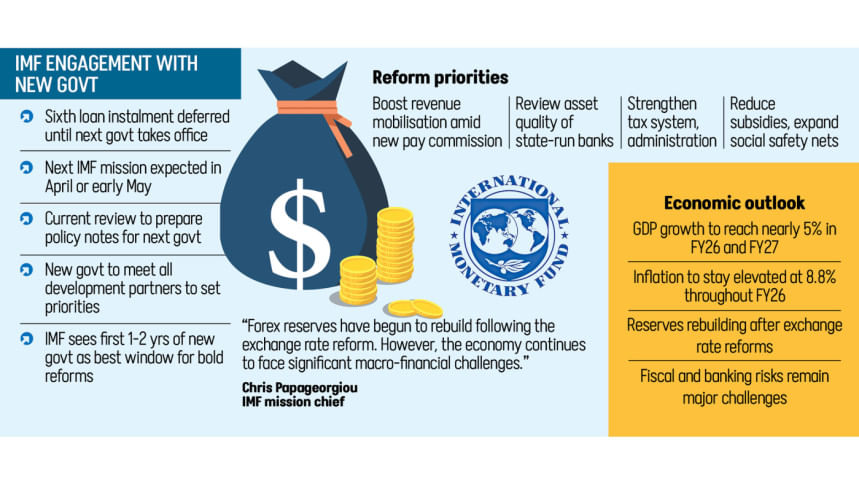

The International Monetary Fund (IMF) will engage with the next government before finalising the upcoming loan review for Bangladesh, said Chris Papageorgiou, IMF mission chief to Bangladesh.

Speaking at a virtual press conference yesterday, Papageorgiou said discussions with the authorities would continue.

"The newly elected authorities, which we are expecting to come into place in February [next year], [will] have an important say in them [IMF reform proposals]," he said.

"So, the plan is that we will continue the discussion, the very strong engagement we have with the Bangladesh authorities in the various different sectors."

The IMF mission, led by Papageorgiou, visited Dhaka from October 29 to November 13 to discuss economic and financial policies under the 2025 Article IV consultation and the fifth review of the IMF's Extended Credit Facility (ECF), Extended Fund Facility (EFF) and Resilience and Sustainability Facility (RSF).

An Article IV consultation is the IMF's annual review of its member countries' economic health.

In a statement, Papageorgiou said discussions on the fifth review would continue in the coming months. "The Fund remains a committed partner to Bangladesh in the quest for sustained macroeconomic stabilisation and strong growth that benefits all its people."

He said talks on the fifth review began during the IMF's annual meetings in Washington.

"So, we felt that we have very ambitious reform targets, and it was important that as we proceed in the programme, we allow for the newly elected authorities, which we expect to come in place in February."

He said the next mission is scheduled for the end of April or early May, and the Fund will re-evaluate whether that would be a combined review.

Earlier, Finance Adviser Salehuddin Ahmed told the media that the next IMF loan instalment might arrive around March or April next year, after the national election, and that this would have no negative impact on the economy.

Asked about the mission team's meetings with political parties, Papageorgiou said the delegation met with Jamaat-e-Islami and BNP to discuss potential reforms.

"These are absolutely needed, and we wanted to hear their views on the programme and what their economic plans are as we move ahead. I think it was a very constructive discussion."

"Both parties are positive about the IMF programme in particular, as well as our collaboration with other IFIs [international financial institutions]," he said, adding that the parties have suggested holding a roundtable with all international financial institutions and development partners after the election to discuss key priorities.

GROWTH OUTLOOK STEADY AT 5%, INFLATION TO DECLINE IN FY27

In its statement, the IMF said Bangladesh's GDP growth in FY25 slowed to 3.7 percent from 4.2 percent in FY24, reflecting production delays during the popular uprising, a tighter policy mix, and heightened uncertainty.

Headline inflation eased from double digits earlier in FY25 but remained high at 8.2 percent in October.

The statement mentioned that the authorities have made progress in maintaining macroeconomic stability by tightening fiscal and monetary policies to contain inflation and reduce external imbalances.

"Importantly, foreign exchange reserves have begun to rebuild following the exchange rate reform launched in May. However, the economy continues to face significant macro-financial challenges stemming from weak tax revenue and undercapitalisation in the financial sector," reads the statement.

The Fund said reforms are needed to create a simpler, fairer tax system and address vulnerabilities in the financial sector.

"With steadfast implementation of these policies, GDP growth is projected to accelerate to nearly 5 percent in FY26 and FY27. Inflation is projected to remain elevated at 8.8 percent in FY26 before declining to 5.5 percent in FY27," the statement said.

"However, downside risks remain significant. Delayed or inadequate policy action in addressing fiscal and banking challenges would weaken growth, raise inflation, and increase risks to macro-financial stability."

Papageorgiou called for ambitious tax reform to generate more revenue for social spending and infrastructure investment. "Potential options include eliminating reduced VAT rates and removing exemptions, except for essential goods and services, and increasing the minimum turnover tax rate for all corporations."

He added that improving tax administration, managing subsidies prudently, and strengthening public financial management would help create fiscal space to support the financial sector and expand social safety nets.

The IMF underscored the need for urgent banking reforms.

"A credible government-wide strategy to comprehensively address weak banks should include estimates of system-wide undercapitalisation, the scope of fiscal support, and legally robust restructuring and resolution options with identified funding sources.

"In addition, asset quality reviews need to be expanded to all systemically important and state-owned banks. Continued efforts are needed to improve banks' governance and balance sheet transparency, strengthen the financial safety net, and improve frameworks for recovering non-performing loans."

On monetary policy, the Fund urged the authorities to maintain a tight stance until inflation falls to the target range of 5 to 6 percent.

"The new exchange rate regime should be implemented fully, including by fostering increased flexibility. To improve monetary policy effectiveness, the authorities should continue to phase out non-standard monetary and quasi-fiscal operations."

The IMF said further structural reforms are essential to unlock growth and make it more inclusive. It acknowledged progress in improving governance of the central bank and fiscal sector, while calling for stronger anti-corruption measures and a more robust anti-money laundering and countering the financing of terrorism framework.

It also highlighted job creation, export diversification, and better macroeconomic data to support policy decisions.

"Building climate resilience and mobilising climate finance remain priorities. Bangladesh has set ambitious goals for achieving environmentally sustainable economic growth," the mission chief said.

He added that progress under the RSF has helped strengthen climate risk management and make infrastructure more resilient to climate shocks. However, more effort is needed to scale up funding and close the climate finance gap.