Weak stocks outpace blue chips in puzzling mismatch

At the Dhaka Stock Exchange (DSE), shares of several little-known drugmakers are trading at prices far above those of local pharmaceutical giants.For example, take the cases of Ambee Pharma and Pharma Aids. Ambee shares are selling for around Tk 780, while Pharma Aids trades at Tk 496. Both feature among the DSE's top-priced stocks.In contrast, the country's largest drugmaker Square Pharmaceuticals sees its shares at Tk 211, nearly four times lower than Ambee and about half the price of Pharma A...

At the Dhaka Stock Exchange (DSE), shares of several little-known drugmakers are trading at prices far above those of local pharmaceutical giants.

For example, take the cases of Ambee Pharma and Pharma Aids. Ambee shares are selling for around Tk 780, while Pharma Aids trades at Tk 496. Both feature among the DSE's top-priced stocks.

In contrast, the country's largest drugmaker Square Pharmaceuticals sees its shares at Tk 211, nearly four times lower than Ambee and about half the price of Pharma Aids.

The puzzle does not stop there -- just with the pharmaceutical sector.

Several loss-making or nearly inactive firms have also climbed into the DSE's list of top-priced shares, leaving established market leaders behind.

What these weak performers have in common is quick capital gains, according to price analyses. But when it comes to dividend payouts, they fall far short of the stronger companies.

Market analysts say this upside-down market reflects speculation and manipulation by groups of individual investors rather than institutional trading. With foreign and asset management investors largely absent, share prices are increasingly driven by rumours instead of fundamentals.

According to DSE data, 360 companies are currently listed on the exchange. Of them, 101 are in the Z, or junk, category -- firms that have either failed to declare dividends or remained closed for years.

Yet 18 percent of these underperformers are trading above Tk 30, while nearly half of A-category companies are priced below that threshold.

WEAK STOCKS, BUT TRADING AT INFLATED PRICES

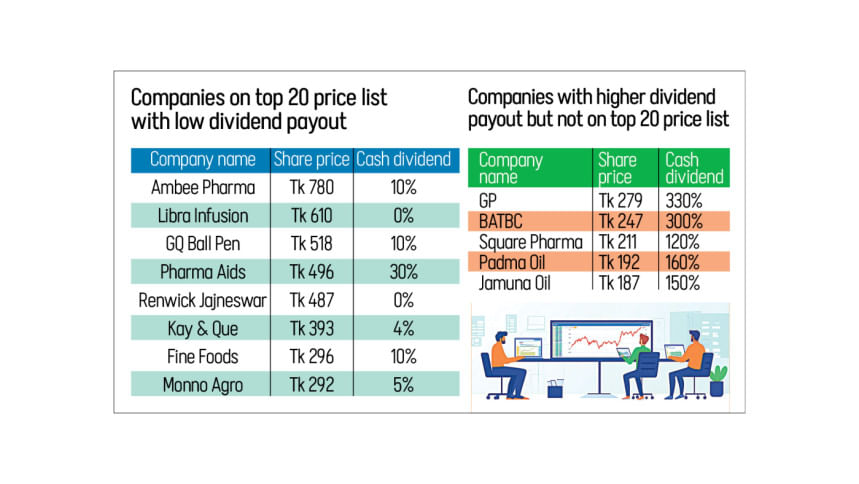

Renwick Jajneswar, a junk stock that has not paid dividends for six years, is trading at Tk 487 and ranks among the DSE's top 20 high-priced shares. The state-owned company manufactures machines and parts for sugar mills.

Intravenous fluid manufacturer Libra Infusion, another junk stock that has not issued dividends since 2022, was being traded at Tk 610 yesterday.

GQ Ballpen, which remains a B-category company, was being traded at Tk 518 yesterday. It paid a 10 percent dividend last year, despite posting a loss of Tk 3 crore.

Another B-category firm, Kay & Que, was at Tk 393 yesterday. It provided a 4 percent cash dividend to its shareholders.

Fine Foods, which offered a 10 percent dividend last year after 1.25 percent the previous year, was being traded at Tk 296.

All these companies were among the DSE's top 20 highest-priced shares.

Meanwhile, large and well-performing firms such as Grameenphone, British American Tobacco, Square Pharmaceuticals, Padma Oil and Jamuna Oil have all been paying over 100 percent dividends for several years. Yet none of their shares feature in the DSE's top 20 list.

Despite the distortions, market records show that strong performers do eventually regain their value, according to market analysts.

"Although many well-performing companies are now trading at low prices, prices do get adjusted after a period," said Kazi Monirul Islam, CEO of Shanta Asset Management. "Sometimes it takes time, but the adjustment happens."

He cited Marico Bangladesh and BRAC Bank as examples of such corrections.

Marico's share price rose 32 percent in the past year due to its consistent performance, while BRAC Bank shares climbed 60 percent year to date till November 3.

Islam said these examples prove that patience and sound fundamentals still matter in the long run.

For discerning investors, he added, the current distortions could even offer opportunities to buy quality shares at low prices.

IN HANDS OF SMALL PLAYERS, AND SYNDICATES

When institutional and foreign participation in the market is low, such price contrasts become more visible, said Shanta Asset Management CEO Islam.

Strong institutional investors, he said, can anchor prices through informed, long-term decisions.

In developed markets, mutual funds and asset management companies play that stabilising role, curbing speculation and bringing consistency to valuations.

In Bangladesh, however, that influence is largely absent, something Islam described as "very unfortunate".

Saiful Islam, president of the DSE Brokers Association of Bangladesh (DBA), said many still confuse banks, insurance firms and non-bank financial institutions (NBFIs) with institutional investors.

"But in reality, asset management companies are the real institutional investors who dominate equity markets in most countries," said the DBA president.

He said that the mutual fund industry in Bangladesh never took off, leaving the market dominated by small, retail players and syndicates of individual investors.

"Had the mutual fund industry been functional, it could have balanced the mismatch between strong and weak stocks," he said.

"What we are seeing now is that small-cap, low-performing companies are being targeted by groups of individual investors because their shares are limited and easy to manipulate," he commented.

The DBA president said the regulator must increase the supply of quality shares and delist zombie companies that fail to pay dividends or remain closed for years.

"Reform is always painful. Surgery cannot be painless, but it is necessary for your health to survive," he said, calling for stricter enforcement to clean up the market.